Available Now

5.00% APY 5-Month CD

Looking for a secure, reliable way to grow your cash savings? Certificates of Deposit (CDs) can help you reach your short-term or long-term savings goals with guaranteed fixed rate returns.

What’s your Goal?

I want to

More Banking Resources

More Mortgage Resources

More Business Resources

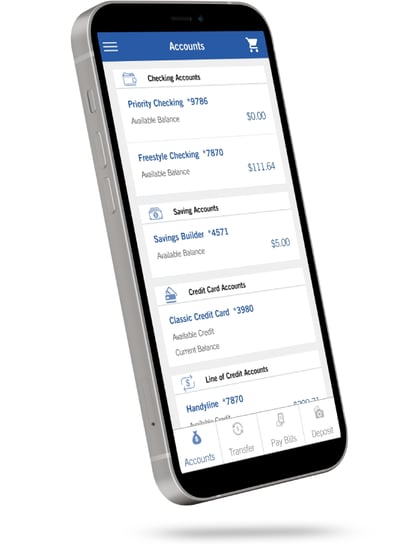

Bank where you want, when you want

Get the convenience of banking on the go or at home, with digital tools that put your account at your fingertips.

Send and receive money with Zelle1

Deposit checks with your smartphone

Shop securely with Mobile Wallet

Pay your bills in one place with Bill Pay

Contact us

About

Resources

Proud to be an official sponsor of

Hancock Whitney Bank, Member FDIC and ![]() Equal Housing Lender. All loans and accounts subject to credit approval. Terms and conditions apply.

Equal Housing Lender. All loans and accounts subject to credit approval. Terms and conditions apply.

Hancock Whitney and the Hancock Whitney logo are federally-registered trademarks of Hancock Whitney Corporation. © Hancock Whitney 2024

![]()